“We get to go through life with our clients. I feel privileged to meet with them and hear about what is happening in their world and with their families. They share their dreams and fears with us, and we get to help them achieve those dreams and conquer those fears.”

Scott infuses everything in his life with care, dedication and a commitment to helping others. As a financial advisor, he serves his clients with wisdom, integrity and kindness, and he has a knack for making complex things simple. He is proud to lead a team of wonderful people and to have helped shape MarsJewett’s culture of service.

A Bellevue native, Scott graduated with honors from Pacific Christian College with dual degrees in Business Administration and Biblical Studies. After college, he spent the first seven years of his career at Boeing. During that time, he and his wife began helping members of their church who were struggling to manage their finances or facing financial crisis, and this helped spark his passion to become a financial advisor. In 1994, he attended a seminar Glenn (Mars) was teaching for the Boeing Management Association, and a year later, Glenn hired him. The rest, as they say, is history.

Scott feels that he truly found his calling as a financial advisor, as it combines his passion for helping people with his love of untangling the technical complexities of finance and investing. He actually gets excited when Congress changes the tax and finance laws, because it means he gets to dig into the research and figure out new planning strategies that will benefit our clients!

Scott is a devoted husband and father of three. Sports are a lifelong passion for him and his wife Kim, and when they’re not watching their own kids play, you’ll likely find them rooting for the Mariners, Seahawks or Huskies—he even proposed to Kim on the 50-yard line of Husky Stadium. Now that his kids are (mostly) out of the house, he has more time to work on his golf game… and he’s quick to say that it needs some work.

Scott is also very active in his community and his church, where he has served for over 25 years in financial ministry. He previously served on the boards of two non-profit organizations, and currently serves on the trust and investment committee at the school his kids graduated from.

When the stock markets are in the news because of a downturn, people often wonder if there is something they should be doing to mitigate the losses. There are several common questions we hear: Is my money dropping like the market? How is my portfolio positioned? How long can I weather a downturn? Is it different this time? Will markets go back up? Let us explore these important and timely questions.

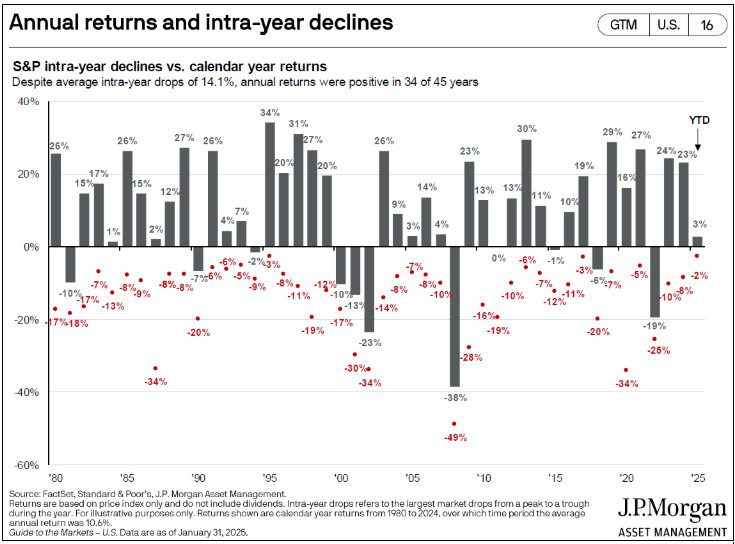

A Look Back

Below is a helpful chart that shows the S&P 500 for the past 45 years, back to 1980. Each gray bar represents a different year and its year-end return. The red dots below each gray bar show how much the market dropped during each corresponding year. Extrapolating from this, we see that markets regularly pull back. Sometimes the drops are small, and sometimes they are quite large. Thus, it is quite normal for the market to experience seasons of volatility, even intra-year.

Thus, it is quite normal for the market to experience seasons of volatility, even intra-year.

What is also noticeable in the chart is that there are far more positive years than negative. In fact, in the past 45 years, there have been just 10 years when the S&P 500 was down at year-end. At the turn of the millennia, another anomaly happened; the market was down three consecutive years in a row. Below you will read why, but that occurrence was a major rarity in the markets.

Is my money dropping like the market?

Thankfully, in this current season of volatility, the models we manage on your behalf are holding up well against U.S. benchmarks. In business cycles, certain market sectors do better than others depending on a multitude of factors. In recent memory, the tech sector has outpaced others, and the domestic stock market has outperformed international markets. Things can change, however, and often do unpredictably. Thus, diversification is a key principle in investing.

Understanding Diversification

To better understand the concept of diversification, imagine an investment portfolio as pie. Each slice represents a different sector of the business economy. There is a slice of U.S. large growth companies, and a slice of large value companies. More slices represent domestic small- and mid-sized companies. So far, this is just the U.S. domestic market. Then, add similar slices for the global stock market, as well as real estate or other specific sectors. Altogether, with each slice representing a different sector, this is diversification. Typically, in a portfolio pie like this, one or more sectors will outperform others. However, predicting the winners is impossible, so it is wise to own everything. This protects assets from overconcentration in one business sector, limiting downside risk when a sector falls.

With recent volatility, diversification is working. A well-diversified portfolio is down much less than the market overall. In fact, as of March 18, international stocks are up as much as U.S. stocks are down. One benchmark representing the global stock market without the U.S. is up over 9% (MSCI ACWI Ex USA). By contrast, NASDAQ’s tech-heavy benchmark is down over -9%. With all the media noise about global concerns and tariffs, could anyone predict international stocks outperform U.S. stock by as much as 18% in early 2025? Thankfully, because the MarsJewett models include international stocks, a diversified portfolio is performing better than a domestic portfolio alone.

How is my portfolio positioned?

As we work within your financial circumstances, and walk together in pursuing your personal goals, we recognize that every person has a different comfort level for market fluctuations. This is known as risk tolerance. Because this is different for everyone, your meetings with us help you identify if your portfolio is positioned right for your risk tolerance and income needs.

When people approach retirement, a portfolio is positioned to provide income for the near-term as well as future needs. This is known as asset allocation. It is the mix of equities (stocks) to fixed income (bond funds and cash). Our objective is to ensure your portfolio is already positioned to provide you with the income needed to supplement what you may already receive from Social Security, pensions, and other sources.

How long can I weather a downturn?

Those needing income from their portfolio typically hold a certain percentage of their money in fixed income assets. Our objective, based on your risk tolerance, is to set aside enough money in bond funds to provide for your needs through a major downturn in markets. When markets drop, we can turn to this fixed income sleeve for income. For example, a person who needs $50,000 annually from their portfolio might have $250,000 in bond funds. This is enough to cover five years of income from bond funds alone.

When markets experience a steep decline, typically they resurge very fast. Stock markets often roar back to pre-decline levels quite fast. Thus, investors who flee to cash sometimes miss the rapid resurgence. Moreover, amidst a decline there is an opportunity to rebalance and shift assets from higher performing sectors into lower performing sectors. This rebalancing takes advantage of stocks when they are down, again leading to better returns on the upside. Tax-loss harvesting in a taxable brokerage account accomplishes this, too, by simply moving temporarily into a similar fund, capturing losses that are used against future taxable gains.

Is it different this time?

Market prognosticators and media outlets love to provoke webpage clicks and viewership. They speak about this time being different. It is natural to worry, and we acknowledge the fear that stems from unforeseen events. Furthermore, like seasons of the past, we are reminded that this too shall pass. We will get through this. Through diversification, a portfolio can weather a rainy season and even participate in outperforming sectors.

For perspective, looking at the 10 years when the market ended down over the last half-century, there was a negative newsworthy event that corresponded with each of those years. In financial industry speak, these are known as “black swan” events, unexpected or out of the ordinary. In 2020, of course, we experienced a worldwide pandemic. In 2008, it was the collapse of the mortgage industry, precipitating the Great Recession. Before that, it was three consecutive events—the 2000 dot-com bubble bursting, the 2001 terror attacks of 9/11, and the 2002 the collapse of Enron—that created a three-year downturn. Most recently, in 2022, markets shook at the duo dilemma of wars abroad and high inflation. In that year, both the stock market and bond market were down simultaneously, which had not happened in 41 years. After each of these unforeseen events, the market roared back. It is tempting to think the worst, but the market roars back as investors take advantage of the opportunity to rebalance and buy into stocks when prices are depressed.

When events cause market to pull back significantly, people draw the same conclusion saying, “it’s different this time.” Looking back, we see most major pullbacks are spurred by one-time, never-before events. Down markets roar back to positive gains.

Will markets go back up?

Returning to the chart at the top of this article, we remind ourselves that markets have a long history. As investors, we are allocated for the long term. We have seen drops before, and we will see drops again in the future. While history is no guarantee of future results, it does help us gain perspective. If the markets go down significantly from here, what then? Learned from previous major declines, we know that human ingenuity does not stop. Progress returns. People in every industry pursue invention, innovation, improvement, and growth of their products, trades, and services.

Disclosures:

The information contained in this communication is for informational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future results. Investing involves risks, including the possible loss of principal. Certain statements in this communication may be forward-looking and based on current expectations or assumptions. These statements are not guarantees of future performance and are subject to risks, uncertainties, and changes in circumstances. There is no assurance that any investment strategy will be successful. Diversification does not ensure a profit or protect against loss in declining markets. The S&P 500 and MSCI ACWI Ex USA indices are used for illustrative purposes only and may not be directly comparable to your portfolio. Index performance does not reflect the deduction of transaction costs, advisory fees, or other expenses that an investor would incur.

Tax-loss harvesting strategies depend on individual circumstances and may not be suitable for all investors. Please consult with a tax professional before implementing any tax-related investment strategy. MarsJewett Financial Group is a Registered Investment Adviser. For additional information about MarsJewett Financial Group, Inc., including its services and fees, you can request the firm’s disclosure brochure using the contact information contained herein or visit advisorinfo.sec.gov. Please consult with your financial advisor to ensure that your portfolio aligns with your risk tolerance, financial objectives, and personal circumstances, as this communication does not take into account your specific investment objectives, financial situation, or needs.

If you are interested in the new numbers affecting 2025 taxes, retirement contributions, health savings, Medicare, and more, please read or download the PDF below to have on hand. As always, do not hesitate to call our office or email us with any questions. 2025 Key...

Artificial Intelligence (AI) has been evolving for over 75 years, starting with Alan Turing’s groundbreaking work in 1950 and the coining of the term "AI" in 1956. Its major breakthrough came in 1997 when IBM's Deep Blue defeated chess champion Garry Kasparov,...

During election season, an overwhelming barrage of messages inundate us. News networks provide an endless supply of political reporting. Video ads stream continually on our televisions, computers, billboards, and devices. It is nearly inescapable. The messages...

If you are interested in the new numbers affecting 2025 taxes, retirement contributions, health savings, Medicare, and more, please read or download the PDF below to have on hand. As always, do not hesitate to call our office or email us with any questions. 2025 Key...

Artificial Intelligence (AI) has been evolving for over 75 years, starting with Alan Turing’s groundbreaking work in 1950 and the coining of the term "AI" in 1956. Its major breakthrough came in 1997 when IBM's Deep Blue defeated chess champion Garry Kasparov,...